New & Used Homes

Browse our full inventory of pre-construction communities and resale listings. Understanding what's available — and the difference between new builds and existing homes — is the essential first move. New construction often comes with builder incentives, warranties, and the chance to personalize finishes before you move in.

Credit Score

Your credit score is the foundation of your mortgage rate — and your rate determines what you pay every month for the next 30 years. Check your score before you apply for pre-approval so there are no surprises. A score above 740 typically qualifies you for the best rates, while scores between 620–739 may still qualify with slightly higher rates.

Repair Your Credit

If your credit score isn't quite where it needs to be, don't give up on your homeownership goals — give yourself a runway. Disputing errors, paying down revolving balances, and avoiding new hard inquiries can meaningfully raise your score in as little as 3–6 months. A stronger score means a lower rate, which could save you tens of thousands over your loan's life.

Get Pre-Approved

A mortgage pre-approval letter is your single most powerful tool when making an offer on a home. It tells builders and sellers you're a serious, qualified buyer — and it reveals exactly how much you can afford. Once your credit is in order, getting pre-approved is the natural next step before you fall in love with a listing.

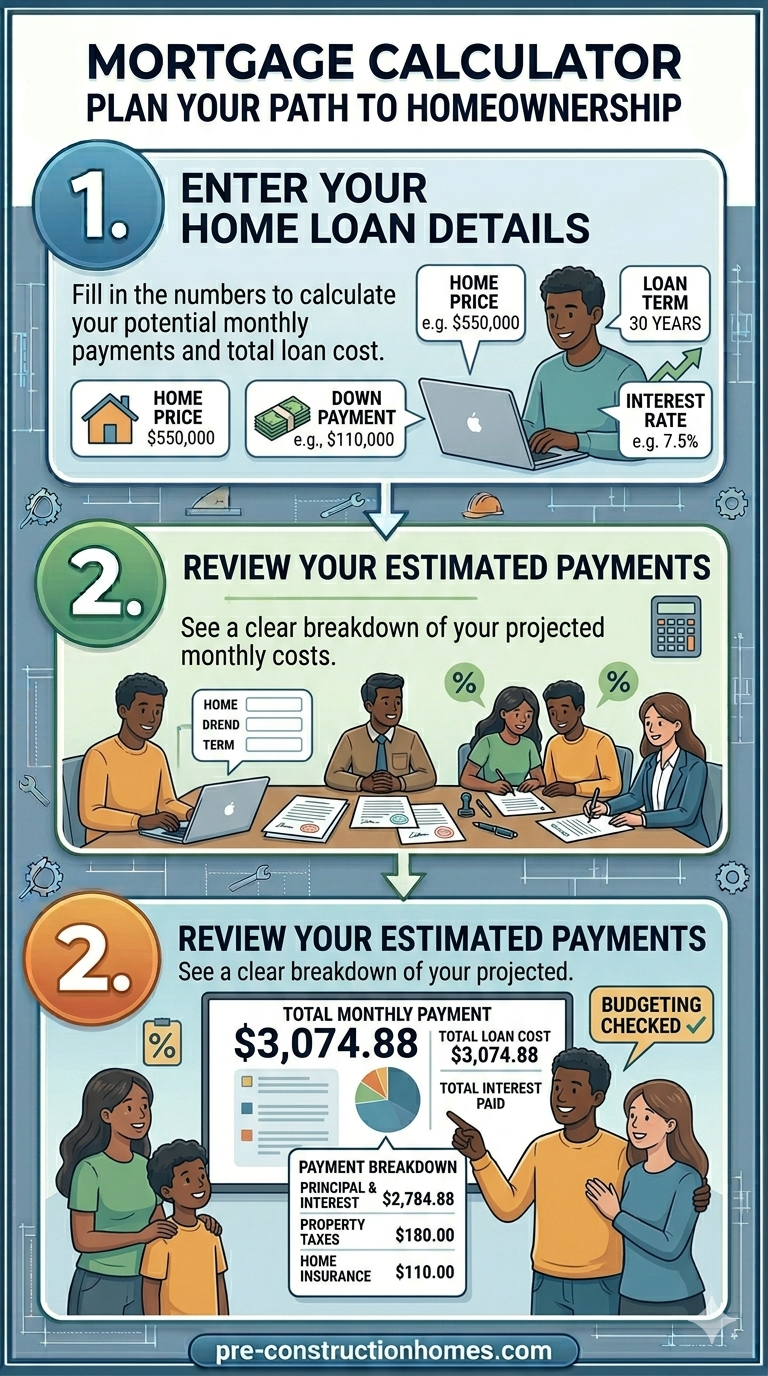

Mortgage Calculator

Before you commit to any listing or builder contract, you need to understand what your monthly payment will actually look like. Our mortgage calculator factors in purchase price, down payment, interest rate, and loan term so you can compare scenarios side by side. Use it alongside your pre-approval to shop within a budget that truly works for you.

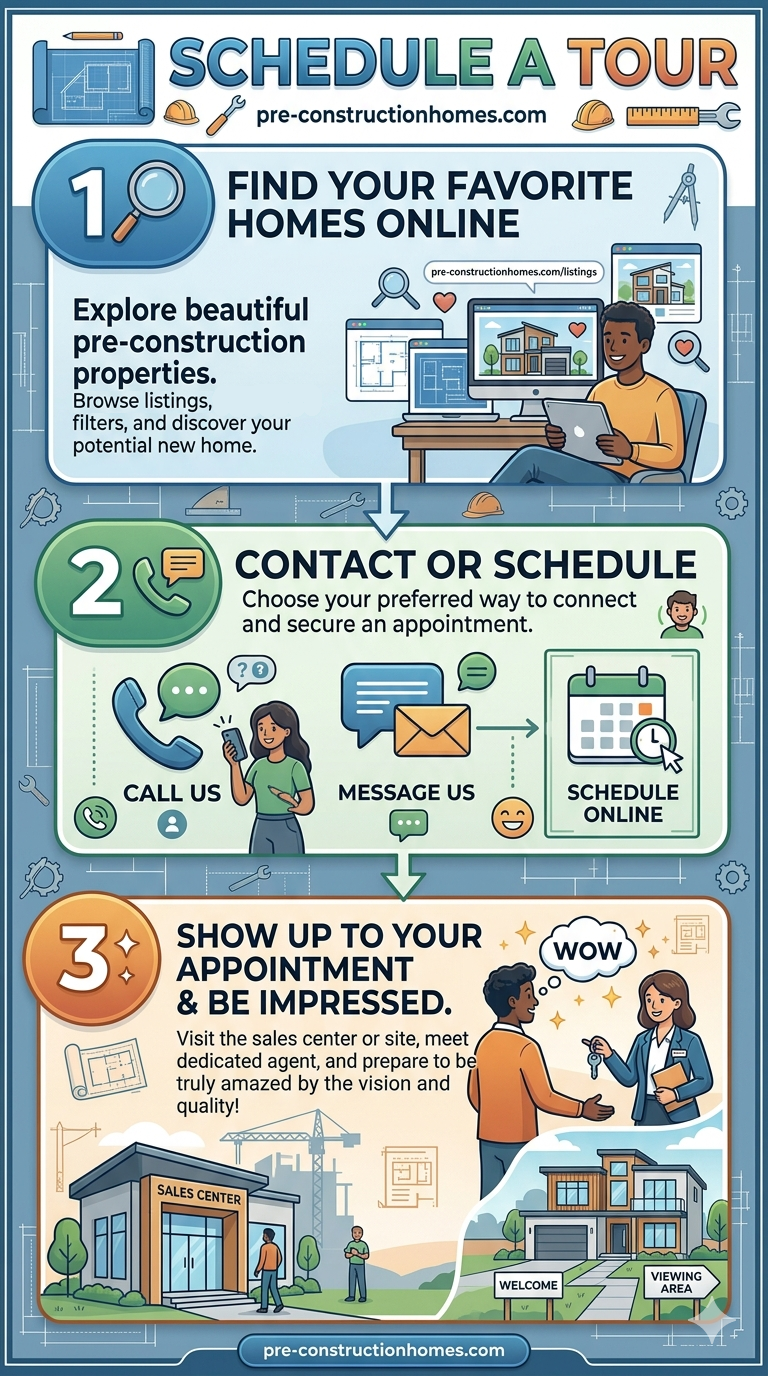

Scheduling Your Tour

Photographs and floor plans tell part of the story. Walking through a model home — or even an early-stage construction site — tells you everything else. Schedule your private tour directly through our platform. Come prepared with questions about build timelines, available lot premiums, and upgrade options to make the most of your time with the builder's sales team.

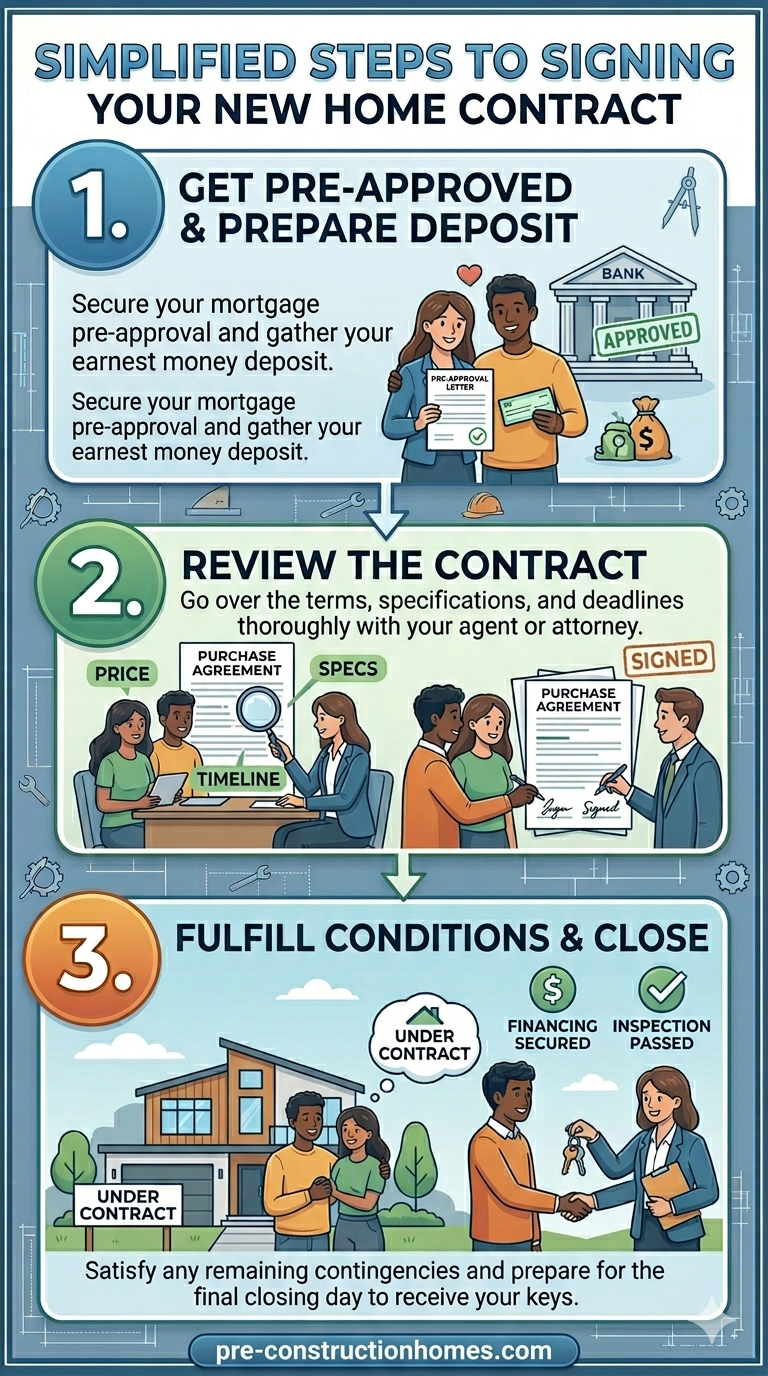

Sign a Contract

After your tour confirms this is the right home, the next step is putting your commitment in writing. A purchase contract (or builder agreement for pre-construction) locks in your price, deposit terms, construction timeline, and included upgrades. Our guide walks you through every clause — what's negotiable, what's standard, and what red flags to watch for before you sign on the dotted line.

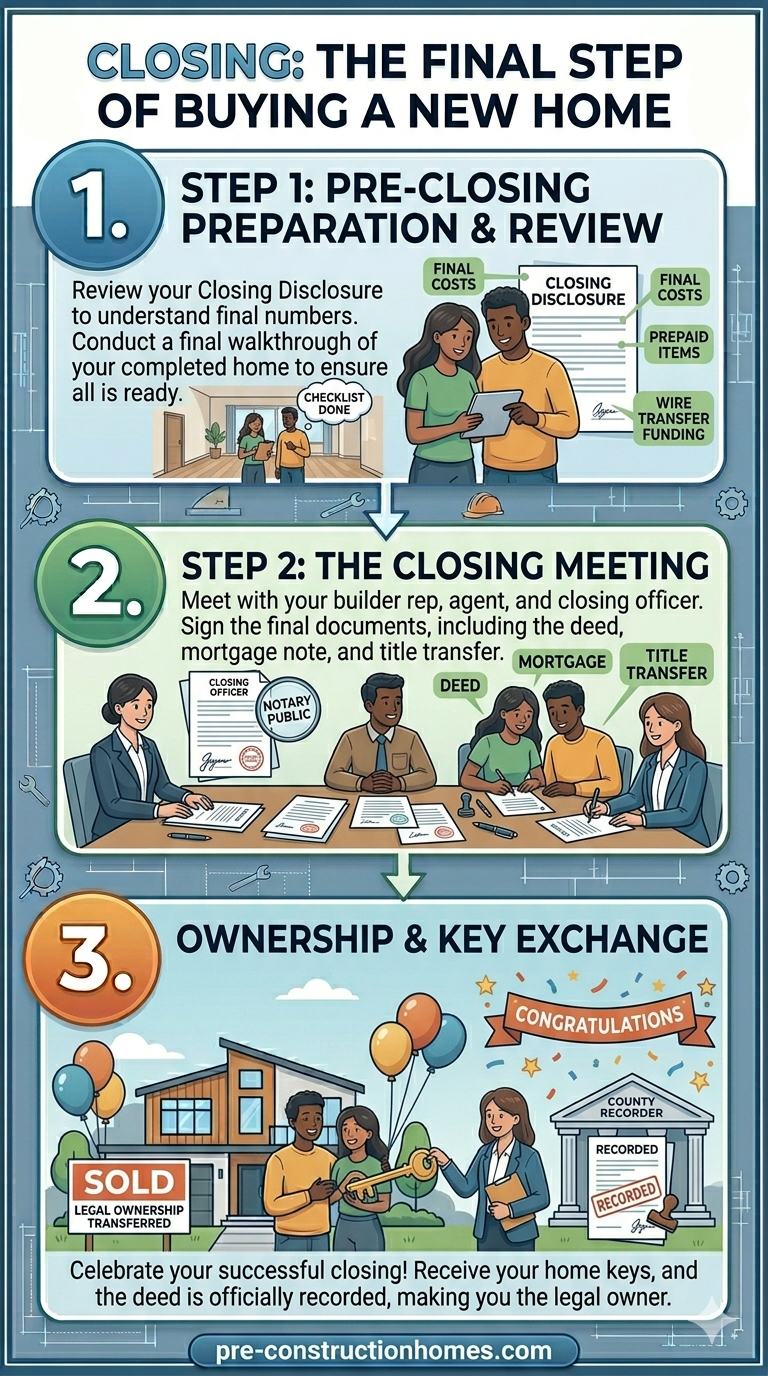

Closing

Closing day is the finish line — and the beginning of everything. This is where you sign the final loan documents, pay closing costs, and receive the keys to your new home. For pre-construction buyers, closing typically happens when the builder issues a Certificate of Occupancy. Our closing checklist ensures you arrive prepared, fully funded, and with zero surprises on one of the biggest days of your life.

Extras

Browse New & Pre-Construction Homes → Anchor Your Budget

Start by exploring listings to understand the price range for the type of home and community you want. This gives you a real-world target to bring to the mortgage calculator and your lender — not a guess.

Check Your Credit Score → Decide Your Next Move

Before talking to any lender, know where you stand. If your score is strong (720+), proceed to pre-approval. If it needs work, take 3–6 months to repair it first. This single step can be worth thousands of dollars in interest savings.

Repair Your Credit → Unlock Better Rates

Credit repair isn't a dead end — it's a detour that pays dividends. Even a 40–60 point score improvement can drop your interest rate by 0.5% to 1%, potentially saving $200+ per month on your mortgage payment.

Get Pre-Approved → Shop with Confidence

With a solid credit score in hand, your pre-approval will reflect your true buying power. Builders and sellers take pre-approved buyers seriously, and in competitive markets, it can mean the difference between getting the home you want and losing it to another buyer.

Use the Mortgage Calculator → Shop Smarter

Run the numbers on each listing you're serious about. Compare a 15-year vs. 30-year term, or model the impact of a larger down payment. Knowledge of your monthly commitment protects you from overextending — and helps you negotiate from an informed position.

Schedule Your Tour → Make Your Decision

Now that you're financially prepared, it's time to experience the home in person. Walk the model, ask about construction timelines, explore upgrade options, and trust your instincts. You've done the work — now enjoy the exciting part.

Sign a Contract → Protect Your Investment

Once the tour confirms your choice, a signed purchase or builder contract secures your price and terms. For pre-construction homes this is especially critical — the contract defines your deposit schedule, build timeline, and what happens if the project is delayed. Understand every clause before you commit, and never skip a legal review if the numbers are significant.

Closing → Keys in Hand

The final step brings every tool in the Toolbox together. Your pre-approval becomes a funded loan, the mortgage calculator's numbers become your actual payment, and the contract you signed becomes the deed in your name. Arrive with your closing checklist complete, your funds wired, and your ID ready — then enjoy the moment you've worked toward every step of the way.